Client champion Martin Lewis’s free instrument for shoppers to probe whether or not they had been victims of discretionary fee agreements (DCA) has logged the submitting of over half one million complaints.

“Final Tuesday,” he wrote in his weekly e mail to subscribers, “we launched our model new automobile finance hidden fee reclaiming information & instrument and… wow! In simply seven days you’ve got despatched over 530,000 criticism emails through it.”

“The regulator,” he provides, “the Monetary Conduct Authority (FCA), estimates 40% of finance agreements had these dodgy fee preparations (you will not know if you happen to did because it was hidden) and the typical payout per association could also be £1,100. In order that probably equates to as much as £234 million coming again to individuals.”

The Cash Saving Professional founder beforehand mentioned he was following the FCA’s evaluation of historic DCAs intently: “We do not consider it doubtless the FCA would do that until it has substantial proof, so a payout is probably going due when it experiences in September. But as claims may very well be time-barred … the earlier you complain, the safer.”

The FCA launched its evaluation after the Monetary Ombudsman Service dominated in two instances that lenders’ DCAs, mixed with an absence of full disclosure to the shopper, had put automobile patrons at a drawback and had been unfair. The FCA mentioned it hopes to rapidly decide if this can be a widespread concern and introduced that it was sending in an unbiased knowledgeable to seek the advice of with automobile loans companies.

Beforehand, Lewis mentioned: “I feel it is extremely very doubtless it’ll rule that there was seismic, systemic mis-selling. A again of the envelope calculation exhibits this can doubtless find yourself being the second largest ever UK reclaim marketing campaign, after PPI.”

“I feel it doubtless that, when the investigation completes (at present deliberate to be September), the FCA will arrange some kind of mass-scale redress scheme – although there is a small probability it’s going to change its thoughts and say this can be a damp squib. One of the best ways to behave is to imagine that scheme is coming.

“Although there is a pause on companies needing to cope with complaints, it’s vital to get your criticism logged sooner, so there’s much less probability you’ll be timed out.”

Lewis reported that the variety of emails despatched to automobile finance suppliers since Cash Financial savings Professional launched its instrument has been unprecedented. “Many companies merely weren’t ready. Nevertheless, lots of the massive companies have assured that they’ll have the ability to acknowledge response of your e mail inside the 28 days. So, if you have not had an acknowledgement but, do not be too involved, they’re doubtless simply swamped.”

Zoe Morton, affiliate director at RSM UK, mentioned: ‘The potential influence of the FCA’s evaluation into discretionary fee preparations is huge, very similar to Fee Safety Insurance coverage (PPI) was, so it’s no shock the FCA has put complaints on maintain for now. Whereas motor finance suppliers and shoppers are successfully in limbo till September, corporations are nonetheless prone to obtain an inflow of complaints, even people who have by no means provided DCAs. This locations them beneath large operational stress.”

She suggested automobile finance companies to plan for the operational influence of coping with these complaints (e.g. useful resource capability), even for these companies who by no means provided DCA, stating that the operational influence by way of coping with these might nonetheless be sizable. “Corporations will nonetheless have an obligation to reply to shoppers, no matter whether or not they used DCA.” she mentioned, including that companies ought to contemplate progressing any DCA complaints already acquired, to make sure instances are adequately ready in anticipation for the decision.

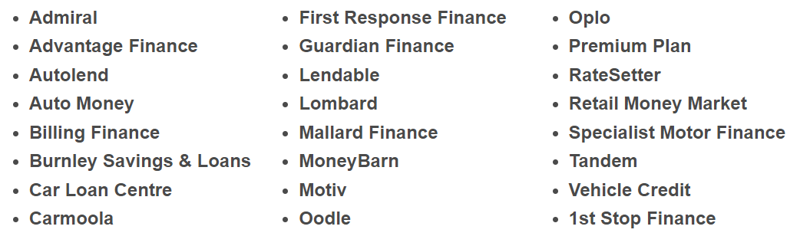

Martin Lewis mentioned that some automobile finance companies instructed his researchers that they’ve by no means used DCAs. “We won’t independently confirm this,” he mentioned, “but it surely’d appear unlikely that regulated companies would make such a blanket assertion until it was true (and if it is not true, we’ll formally complain to the FCA about deceptive data).

“So in case your automobile finance was with any of those companies, it is most likely not price making a declare. The present record is…”

The FCA lately mentioned it has gone into the evaluation with no prior assumption of what it’s going to discover.

The FCA lately mentioned it has gone into the evaluation with no prior assumption of what it’s going to discover.